The recent BC Budget projects a deficit of $13.3 billion for the coming year. As part of the Budget process, most branches of government, including the BC Liquor Distribution Branch (LDB), provide updated fiscal plans for the coming years. The LDB has posted its Service Plan for 2026-2028 here.

The Service Plan predicts a challenging environment for liquor sales in BC over the next few years with flat revenue and increased operating costs. This will have significant consequences for the government revenue that derives from liquor sales. Indeed, the annual LDB contribution to government revenue is projected to decline significantly in the coming years, down substantially from a pandemic era high of $1.193 billion in the 2021/22 fiscal year to just $847.3 million in the year ending in 2029.

The table below shows comparisons for the 2021/22 fiscal year, projected numbers for the current 2025/26 fiscal year, and for the 2028/2029 fiscal year. It also adds per capita amounts of liquor revenue for each year based on government population projections.

BC

2021/22

2025/26

2028/29

Change 2022-2029

Revenue

3.751b

3.620b

3.742b

0%

Net Income

1.193b

950m

847.3m

-29%

Per Capita Amount

222.69

168.41

151.38

-32%

For British Columbia, and if the projections are correct, the table shows fairly flat gross sales over a 7 year period (which would mean a decline in volume), with a decline in net income of -29% in absolute dollars and -32% in per capita revenue. During the same time period, operating expenses rose by 34% from $508m to $680m. For comparison, and for the 6 year period ending in 2028, Alberta is projecting smaller declines of -6.7% (absolute dollars) and -19% (per capita).

The Service Plan indicates that some of the contributing causes to these declines are:

BCGEU strike action in the 2025/26 fiscal year

Removal of U.S. liquor products from the LDB system

Reduced consumer demand for alcohol including health and lifestyle concerns

General economic conditions

Decline in immigration levels

Increased expenses including those related to collective agreements

Yesterday, the Conservatives put forward a private member’s bill (Bill C-262) that was described as being a solution to Canada’s national problems with interprovincial alcohol shipment (DTC). The proposal is described more fully here: Conservatives Want To Make It Easier to Mail Alcohol Between Provinces. You can also read the actual text of Bill C-262 here. Internal Trade Minister Dominic LeBlanc even said that he thought the idea was a “good one”.

While I support both the spirit of this effort and the ability of Canada Post to deliver alcohol between provinces, it seems to me that this Bill is not an adequate solution … and could create additional problems for affected wineries. My thoughts on this are as follows.

Firstly, as far as I can tell, there is nothing in the current legislation that governs Canada Post that prevents it from delivering alcohol between provinces. Indeed, Canada Post has a policy on the delivery of intoxicating beverages that states that they will currently make interprovincial shipments so long as the shipper complies with the relevant provincial laws. It is the combination of the relevant federal (Importation of Intoxicating Liquors Act) and provincial laws that creates the legal DTC problem … not the Canada Post Corporation Act.

The real problem is that there are still a number of provincial laws that make it either illegal for the customer to receive the interprovincial shipment or which impose such onerous obligations on the customer and/or winery as to make it impractical.

Bill C-262 doesn’t make any substantive changes to this legal structure … other than to explicitly state that Canada Post must provide an alcohol delivery service … and gives them an initial monopoly on doing so. In other words, it addresses the choice of ‘transport’ of the shipment rather than the overall legality of the entire transaction. It’s the latter issue that needs to be addressed to fix the problem.

At a recent AIDV webinar, a panel of experts brainstormed this issue. One of the ideas was for the federal government to proactively create a national exemption for personal shipments of alcohol between provinces. This should be done under the Importation of Intoxicating Liquors Act … which is the federal legislation that governs the trade in interprovincial and international alcohol (rather than the Canada Post Corporation Act). While there could be legal challenges, this would arguably (and practically) have the effect of over-riding provincial restrictions since the federal government has the exclusive jurisdiction under our Constitution to make laws regarding interprovincial trade.

Essentially, this would create an “internal duty-free exemption” similar to the one that is in effect at our international border for returning travellers. Canadians would be able to order and receive specified quantities of alcohol from other provinces without worrying about interference from their local liquor monopoly … a concept that works well nearly everywhere else in the world.

Indeed, this model has been working splendidly since 2012 in Manitoba where its residents have enjoyed the freedom to order alcohol from other provinces for years … without any apparent significant issues … and without any noticeable effect on provincial liquor revenues.

A national personal exemption would accomplish this and fix the problem properly. Here is my first draft of an amendment to the Importation of Intoxicating Liquors Act that could potentially fix this.

Personal Exemption

9. Notwithstanding any other Act or law, a person is permitted to import, or cause to be imported, into a province from another province an amount and type of intoxicating liquor for personal consumption that is specified by regulation and in a frequency and manner specified by regulation.

Personal Exemption Regulation

1. For the purposes of s.9 of the Act, the amounts and types of intoxicating liquor for personal consumption that are permitted are, for each person:

a) x litres of wine;

b) x litres of beer; and

c) x litres of spirits.

2. The amounts and types of intoxicating liquor specified in section 1 may be imported by each person in any 30 day period and either by in-person importation or by delivery by any common carrier from the other province.

Secondly, I do not understand why Bill C-262 proposes to give Canada Post an initial monopoly on interprovincial shipments of alcohol. Most wineries in BC do not currently use Canada Post as their preferred shipper. There are many reasons for not doing so … one of the most important of which is that they do not use temperature controlled trucks.

The Bill contemplates adding “trusted” carriers eventually … but why should those carriers have to go through a bureaucratic approval process to get the ability to do something that they are already doing well right now? If passed, the Bill would effectively prevent existing carriers from delivering alcohol until they got approval as a “trusted carrier” through some yet to be created bureaucracy. The last thing Canadian wineries need right now is to grant another ‘monopoly’ on anything liquor related to a branch of government.

So to conclude, while any discussion of these issues at the national level is helpful, I do not think that Bill C-262 solves the problem. Instead, let’s consider a national personal use exemption … and let any current common carrier make those deliveries.

On March 2, Ontario and Nova Scotia announced a deal that would enable wineries in each province to ship and sell direct to consumers in the other province. In other words, a ‘reciprocal’ deal to permit DTC … almost 2 months in advance of the target date of May 1st to resolve these issues that the federal government had previously announced.

The details of the arrangement were not provided in the news releases that each government issued. However, additional information is now available on the web sites for these provinces: LCBO (Ontario) and NSLC (Nova Scotia).

In each province, wineries will need to apply for and receive an authorization from the relevant liquor authority. They will also need to remit markup and sales taxes on a quarterly basis.

For Ontario wineries wishing to ship and sell to Nova Scotia customers, the NSLC site indicates that a “5% fee on total retail sales” will be charged (presumably plus sales tax). See this page on the NSLC site.

For Nova Scotia wineries wishing to ship and sell to Ontario customers, the LCBO site does not clearly state the relevant markup level … but these are contained in the sample templates which can be downloaded on this page.

Apparent Typo of 1.6% Markup for DTC (also LCBO spelled wrong!)

Templates are provided for wineries, distilleries, and breweries. The winery template states that the LCBO markup is 1.6% for Canadian wine … which appears to be a typo … because the current LCBO markup for Ontario wineries is 6.1%. It would appear that the intention is to treat out of province wineries the same as in-province wineries (which would be compliant with the reasoning in the SCC Comeau decision).

Various other markup amounts are indicated for other products: e.g. 20% for “wine coolers and other wine” … and 32.5% for spirits.

These initial indications show some potential for national DTC because, while there is an additional administrative burden, they appear to be indicating that the liquor boards are prepared to reduce their ‘normal’ markups to much more reasonable levels for out-of-province producers … treating them the same as an in-province winery. For example, a 6.1% markup on a $40 bottle of wine would be $2.44. Regrettably, they are still focused on percentage based markups rather than volume-based ones (like Alberta).

Unfortunately for BC wineries, no such deal has yet been announced between BC and Ontario. In this regard, BC currently charges zero markup to Ontario wineries shipping to BC … but Ontario currently does not permit any shipments at all to Ontario consumers. I note that the BC system requires no additional administration or registration for the winery … while the ON/NS model requires registration and quarterly reporting (which, if extended, could mean doing so for all participating provinces).

Fingers crossed that all of this will be resolved promptly … and perhaps before May 1st.

In addition, I note that the above system could potentially form the basis for an international trade compliance challenge under GATT or other applicable trade agreements since domestic wine is treated much more favourably than imported wine (if we even care about such compliance any more).

The Alberta government introduced its 2026 budget today and indicated that it would remove the percentage based tax on “high value” wine that it implemented last year: see page 61-62 of this budget document which states that the tax will be removed because it created “reduced transparency and business uncertainty”.

The percentage based tax was complicated and received intense criticism from industry (see: Alberta Hikes Wine Markups). It also hindered efforts at resolving direct to consumer shipments of wine between provinces since it was almost impossible to administer for wineries in other provinces.

Instead, the Alberta government has indicated that they will revert to the volume-based liquor markups on wine that they have used for many years. The budget document indicates that this markup will increase by $0.58 per litre. As the previous rate was $4.11 per litre for most wine, the new rate will presumably be $4.69 per litre (which would be $3.52 for a 750 ml bottle).

This change is good news for Alberta food and wine culture … and for wineries in other provinces such as BC.

Last week, the US federal government updated its dietary guidelines for Americans including its recommendations on alcohol consumption. The update suggested that consuming less alcohol is better for “overall health” than drinking more but also removed specific numerical drink limits implying that moderation should be an individual assessment. At the same time, the US Congress House Oversight Committee released a report entitled “A Study Fraught With Bias” (the Congress Report) that was sharply critical of one of two study projects that aimed to shape the update including specific condemnation of Canada’s alcohol and health “model”.

The first US study had been authorized and funded by Congress and was known as the NASEM Study (National Academies of Science, Engineering, and Medicine). The second effort was known as the AIH Study (Alcohol Intake & Health) which was undertaken by the Interagency Coordinating Committee on the Prevention of Underage Drinking (ICCPUD). The AIH Study was a competing effort which raised eyebrows from inception. It was not clear why or how it was authorized since ICCPUD’s mandate is underage drinking, not dietary guidance … and Congress had specifically authorized NASEM to provide the relevant advice. In addition, 3 of the 6 AIH Study Group members were academics working in Canada.

Felicity Carter provides an excellent analysis of the details of the studies and the political intrigue surrounding them here: It’s Not No Safe Level – But Not Moderation Either. From a high level, the new US dietary guidelines on alcohol seem reasonable (and acceptable to the wine industry) since they did not accept the “no safe level” arguments that have been put forward by anti-alcohol advocates recently.

From a Canadian policy perspective though, there is much of interest in the Congress Report since it directly criticizes the “Canadian model” of guidance for alcohol and health (by which they mean the 2023 CCSA Recommendations that have previously been commented upon in this blog). Specifically, and while parts of the Congress Report were partisan in nature, it made the following findings of fact:

The AIH Study was “conducted in a manner inconsistent with federal law” and “is irretrievably flawed”. The six members of the AIH Study Group were determined to be “fraught with bias” since they were all “anti-alcohol advocates with beliefs predating the study that no amount of alcohol consumption is safe, contrary to several accepted studies in the field”.

The three Canadian members of the AIH study group “were affiliated with creating the ‘Canadian model’ study that concluded that no amount of alcohol consumption was safe” (the 2023 CCSA Recommendations).

The composition of the AIH study group was deliberately designed to reflect “the goal of the study: begin with a pre-determined conclusion that no amount of alcohol consumption is safe and recruit biased scientists to develop the research to support that conclusion.”

The three ‘Canadian’ members of the 6 person AIH Study Group were: Kevin Shield, Timothy Naimi, and Jurgen Rehm. The first two members (Shield and Naimi) were part of the group that produced the 2023 CCSA Recommendations, which included numerous references to the work of the third member (Rehm).

What is one to make of all of this … and particularly the direct rejection of the “Canadian model” and CCSA Recommendations? The first and most obvious observation is that the objectives and process for producing the US drinking guidelines is quite different from the objectives and process that Health Canada has used to inform its “Low Risk Drinking Guidelines”.

In the US, the drinking guidelines have formed part of the broader US Dietary Guidelines which are legally required to be created “based on the preponderance of the scientific and medical knowledge which is current at the time the report is prepared”. As such, Congress authorized NASEM to advise on alcohol consumption and assembled a broad panel of 14 medical and public health experts to consider the issues. The credentials of that panel are top-notch including representation from some of the leading universities and hospitals across the country (e.g. Harvard, Cornell, Brown, Stanford, Johns Hopkins). That group concluded with “moderate certainty” that those who drink in moderation have lower all-cause mortality than those who don’t. This was in stark contrast to the much smaller AIH Study Group who wrote in a draft that “the risk of dying from alcohol use begins at low levels of average use”.

In Canada, and in contrast, Health Canada commissioned the Canadian Centre on Substance Abuse and Addiction (CCSA) to provide recommendations for its standalone drinking guidelines which are not published as part of general recommendations for a healthy diet. I note that every single one of the purposes of the CCSA (which are set out in its governing statute) relate to addressing “alcohol and drug abuse”. None of their mandate relates to general dietary issues or to lifestyle or to exercise or toward normal alcohol consumption that is not related to “abuse”.

In other words, the CCSA is funded by government for, and devoted to, addressing issues of addiction and abuse. This is no doubt a noble cause and is important work. They would be exactly the right people to ask about consumption advice for those with a history of alcohol abuse problems. However, I don’t think that this process could be expected to provide reasonable consumption advice for the vast majority of Canadians who drink in moderation and do not “abuse” alcohol.

The second observation is to look at how the experts were chosen, the diversity of representation, and ask whether or not there was any bias that might influence their advice. Again, the US approach differs significantly from the Canadian one. As the Congress Report pointed out, the NASEM group was diverse and from highly respected institutions. In contrast, the AIH group was smaller and the Congress committee found that they had been picked precisely because they shared common anti-alcohol views and a “no safe level” perspective.

If we look back at the 2023 CCSA Recommendations, we can see that they were produced by a relatively large group of 22 panelists. While some are from well known Canadian universities, the majority are either addiction professionals or otherwise connected to addiction treatment. A few have spent their entire professional careers engaged in anti-alcohol advocacy (usually at taxpayers’ expense). As such, there was little apparent diversity in representation or viewpoints. Given the findings of the Congress Report, one must ask whether or not a similar thing happened in Canada as at the AIH Study Group: were panelists picked because they were “anti-alcohol advocates with beliefs predating the study that no amount of alcohol consumption is safe”?

If the above is correct, perhaps we can understand why the CCSA recommendations are so different from the US guidelines and why they were rejected by the Congress Report. If you ask a group of ‘experts’ who specialize in addiction and abuse what a safe level of drinking is … then they will likely respond “none” or that there is “no safe level” … because that is probably the right answer for an alcoholic or an addict. These ‘experts’ will have a perspective that is created by their professional experience. In that sense, the Congress Report might be right … they have a bias that is based on addiction and abuse. If you ask a different group of experts who specialize in general health the same question, you will likely get a very different answer … which is what happened at NASEM.

Significant policy questions remain for Canada. Which is the right approach to generate drinking guidelines? Do the findings of the Congress Report also imply that Canada’s “model” is “irretrievably flawed” and “fraught with bias”? It appears to me that many of the criticisms in the Congress Report are valid in respect of the Canadian “model”. Why is Health Canada asking the CCSA (an organization devoted to dealing with alcohol abuse) and a panel of addiction experts to generate drinking guidelines for normal folks who don’t abuse alcohol … which is most of us?

Canada appears to be experiencing a resurgence of Prohibition era thinking which is based on the assumption that any consumption of alcohol is likely to lead to extensive problems for everyone regardless of context. Indeed, the comical recommendation of the CCSA that drinking should be limited to 2 drinksper week creates a significant conflict of interest for them and for Health Canada: the threshold for “abuse” would be set so low that the CCSA can justify asking for even greater taxpayer funding since the entire drinking population would effectively become within their mandate.

This does not seem like an appropriate way to create government health policy … or to spend taxpayer dollars for the vast majority of Canadians. And, sadly, it may have taken a report of the U.S. Congress to point that out.

The BCLDB (the government wholesale liquor monopoly) releases a quarterly Liquor Market Review, which often contains useful information on wine sales and trends in the BC marketplace. They recently released the review for Q2 of 2025-2026 which covers off the sales period from July-September 2025. Compared to the previous year, wine sales declined by 2.3% for this quarter (about $7m in value on total sales of $289m).

During this time, the BC Government maintained a direction to BCLDB wholesale to stop importing US alcohol products and to remove such products from the shelves of BC Government liquor stores. Existing stock remained for sale in private channels (e.g. private retailers, bars, restaurants). Compared to a year earlier, sales of US wines dropped dramatically during this quarter – down over 73%.

Where did those customers go? The recently released numbers show that those customers mostly continued to buy wine (although sales were down just over 2% as mentioned) … and that mostly they switched to other import countries. Here are the statistics for the larger wine regions.

Country

2024 Q2 (000s)

2025 Q2 (000s)

% change

Argentina

5987

7346

+23%

Australia

10110

11695

+16%

Canada BC

146626

149039

+1.6%

Chile

10723

11681

+8.9%

France

25769

27587

+7%

Italy

28195

30027

+6.4%

NZ

13386

15307

+14%

Spain

5406

6151

+14%

USA

28390

7547

-73.4%

Here are a few observations from the above numbers.

– Firstly, there’s only a small 1.6% sales increase for the “Canada BC” category. In the previous quarter, this category had logged a 6% sales increase. However, I note that the BCLDB includes both “blended in Canada” wines (made from imported grapes/juice) and 100% BC wines in this group, so that complicates the analysis. The sales numbers for 100% BC wine, and for individual wineries, may be different. These numbers are further complicated by the presence of vintage replacement wines (mostly made from U.S. grapes) in the marketplace.

– Some countries have been big winners … notable sales increases for Argentina, Australia, New Zealand, and Spain … with smaller increases for Chile, France, and Italy. This should obviously worry US producers as it may be hard to get these customers back once the trade issues get resolved.

– Local importers who were able to bolster their losses in U.S. sales with increases from their non-U.S. winery clients may have been able to survive a tricky quarter … but importers whose portfolios were more dependent upon U.S. sales will have experienced a very challenging economic quarter. There is no doubt that some importers will have had to take drastic action as a result, particularly as large amounts of U.S. inventory are generating few sales.

– The continued decline in overall wine sales (down again by over 2%) is worrying for the wine industry overall. Whether this is due to changing demographics, general economic worries or health concerns, it is troubling to see erosion in a market that once saw continuous growth.

– The above figures are for wholesale sales … they are probably also representative of retail sales but there could be some differences.

My recent review of alcohol sales and government liquor tax revenue reveals some interesting points which may have implications for future liquor tax policy across Canada and elsewhere. Canada’s provincial governments have relied upon liquor revenue to contribute to their general operations since Prohibition. However, that reliability appears to be threatened as declining consumption and high prices are now resulting in falling levels of liquor revenue on a per capita basis in certain places.

Statistics Canada tracks the amount that government makes from liquor sales across Canada and provides continually updated data here, which can be segregated by year and by province. Here are the total liquor board contributions to government revenue for the most recently available 3 annual periods and for four select provinces. I have added “per capita” contributions to provide a point of reference comparison (I used general population, although I suppose it could arguably be more useful if this was limited to drinking age).

BC

2021/22

2022/23

2023/24

Liquor Revenue

1.193b

1.193b

1.130b

Per Capita Amount

222.69

216.31

199.25

AB

Liquor Revenue

854m

825m

791m

Per Capita Amount

189.23

175.94

161.13

MB

Liquor Revenue

322m

327m

323m

Per Capita Amount

227.88

225.05

216.49

ON

Liquor Revenue

2.543b

2.457b

2.574b

Per Capita Amount

167.79

157.17

159.43

There are some interesting takeaways that can be extracted from the above.

– Overall, annual government liquor revenues are fairly flat despite these years being fraught with inflationary pressure. But in AB, revenue is actually down by about 7%. The “per capita” amounts of government liquor revenue have also mostly decreased. In BC, revenue is down on a per capita basis about 10% over 2 years. In ON and MB, it’s down about 5%. But in AB, it’s down almost 15%.

– The above may explain AB’s recent introduction of a contentious “high value” percentage based wine tax … as an attempt to boost revenue. But this seems a particularly ham-handed way to do it as the most reliable way to increase revenue would be to increase the flat (volume-based) tax on all alcohol, not just target wine in a complicated way that makes the tax almost impossible to administer. My guess is that they will not increase revenue by the amounts that they want and will have to revisit this approach.

– Manitoba, which is the only Canadian province, to have completely open borders for interprovincial DTC (direct to consumer) alcohol shipping, has the highest amount of per capita liquor revenue of all of these four provinces. This may be partially due to high MB liquor markups but, regardless, it confirms my belief that the DTC issue will not significantly affect provincial liquor revenue. Indeed, the province with the most open borders actually has the highest revenue!

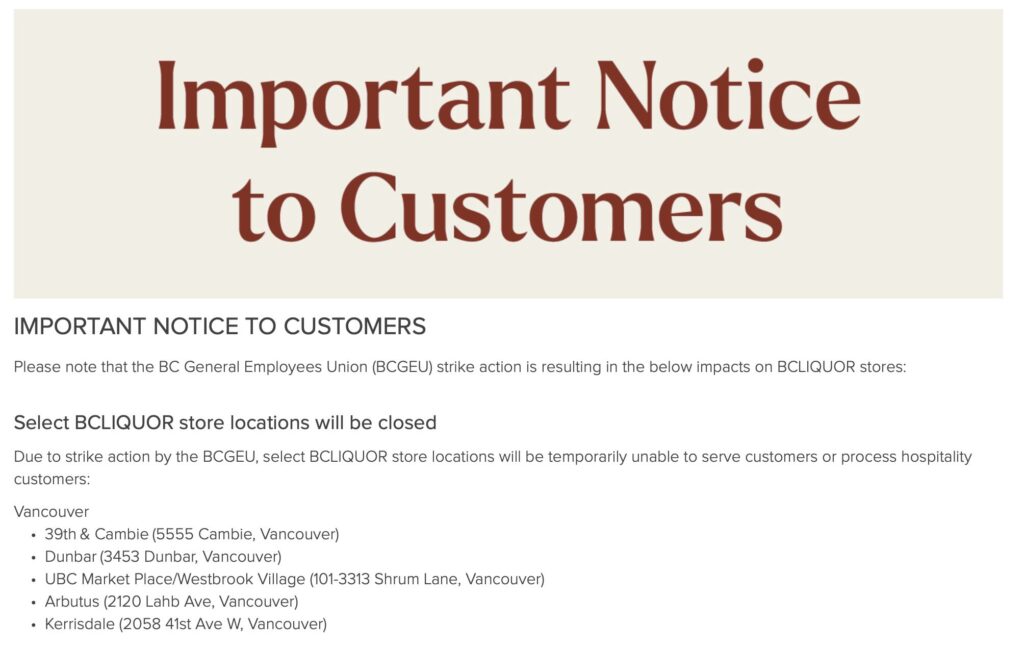

British Columbia’s government controlled liquor distribution system (BCLDB) is now in crisis mode due to a strike by the BCGEU which has now shut down all of the government liquor distribution warehouses and a significant number of high volume government retail stores. The complete shut down of the system will have serious knock-on effects for restaurants, bars, hotels and private retailers, all of whom depend upon the BCLDB for their import liquor supply and associated revenue. The crisis is made worse due to hang-over economic effects from the pandemic, reduced overall consumption, and from the province’s ban on the importation of U.S. alcohol.

A few of the immediate consequences are as follows:

Restaurants, bars and hotels will soon run out of import inventory on some of their most popular liquor products as it will be impossible to replenish inventory.

Private retailers will also face challenges if the strike drags on as they too will be unable to replenish inventory.

The business of import agents (mostly small local companies) is effectively suspended since they have no way of getting their product out of the warehouses where they are stored.

Special events, including charitable ones, will have trouble sourcing liquor supplies and some may have to cancel.

Saturday’s Bordeaux release event at government BCLS stores looks in jeopardy as most of the major stores are now shuttered.

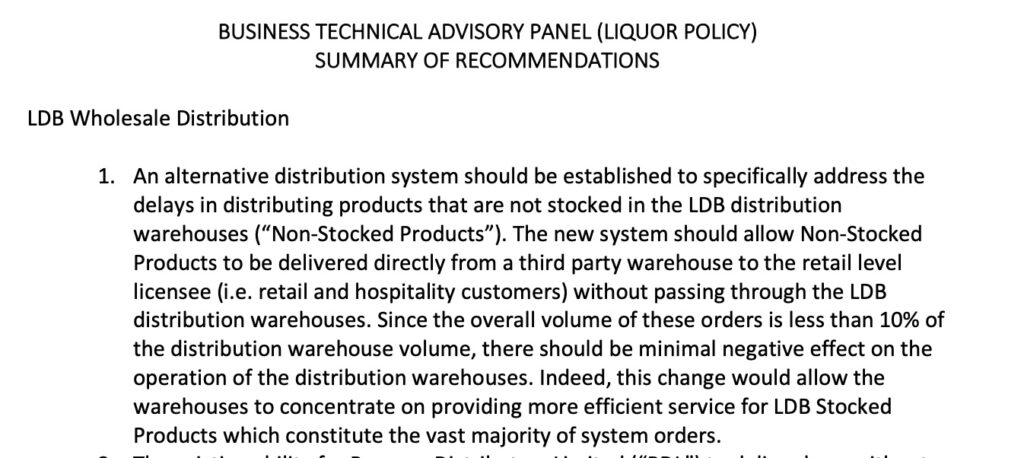

It is particularly unfortunate that previous government efforts at liquor policy reform have failed to address some of the fundamental problems with the system, leaving in place structural flaws that have been around since after Prohibition. Specifically, we need to fix the following problems urgently.

Government Warehouse Bottlenecks. BC still requires that all imported alcohol be distributed through government warehouses in Delta or Kamloops. This applies even when the alcohol is primarily stored in a separate third party warehouse (which most of it is) and even when the alcohol is being delivered to a non-government licensee (e.g. restaurant, bar or private retailer). The forced requirement for a government “middle-man” is neither efficient nor environmentally sustainable. It increases costs and causes a complete breakdown in distribution whenever there is a strike (or any other disruption to the operation of the government warehouse). There is simply no reason for this system to continue. Indeed, this problem was the subject of Recommendation #1 in the 2018 BTAP Report (which I authored on behalf of the wider industry stakeholder group). Our modest proposed change was not implemented by government. If that change had been made, the system would not have ground to a halt as it has today.

BTAP Recommendation #1

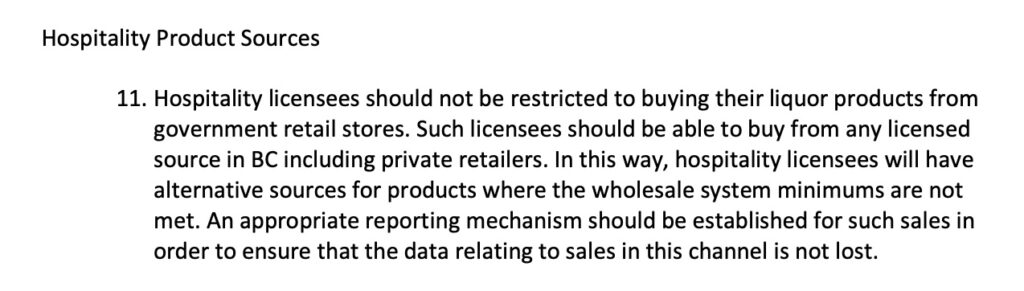

Licensee to Licensee Sales. BC also still requires that hospitality licensees (restaurants, bars, and hotels) can only buy their import stock from LDB Wholesale or from a single designated government liquor store. Both of those options are now out of commission for most licensees. The only practical option (buying from private retailers) remains illegal. This too must change. Even when the system is working, it is unacceptable that it is illegal for a restaurant to buy a few bottles of wine from a nearby retailer if it has run out of something. It is utterly scandalous, that it remains illegal when the restaurant has no choice because the system has shut down. Again, this was the subject of Recommendation #11 in the 2018 BTAP Report. Again, our modest proposed change was not implemented by government. If that change had been made, then hospitality licensees would at least have some options and flexibility in trying to survive.

BTAP Recommendation #11

These are the two most prominent examples of badly needed change … and there are more. Government needs to finally fix some of these issues once and for all. Kicking the can down the road repeatedly no longer works. Prohibition in BC ended in 1921 … why are we still using and accepting aspects of a government control system for liquor that should have been modernized decades ago?

I have sometimes told a joke when I am speaking at wine and liquor law events: “there are two speeds for liquor policy change in Canada – glacial and backwards”. Sadly, the current political situation regarding the internal trade barriers for alcohol sales is proving that our provincial politicians regard the “glacial” description as absolutely appropriate for their “efforts” in this area.

To summarize, in February of this year, Federal Minister of Internal Trade stated that Canada would have its internal trade barriers regarding alcohol removed “within 30 days”. Prime Minister Carney later revised this optimistic time estimate and stated that the job would be done by “Canada Day” (July 1st).

Yesterday, Canada’s Committee on Internal Trade issued a press release “Committee on Internal Trade Meets to Strengthen Canada’s Economy” in which they happily informed us that most of the provinces (Newfoundland is a hold-out) have signed a Memorandum of Understanding to start work on a national system for direct to consumer sales of alcohol that is slated to be rolled out by May 2026. You read that correctly … no announcement of legislation, no firm commitments, no framework of an agreement … they have signed a “memo” in which they agree to start work on this … and perhaps finish that work by the middle of next year.

This is a stunning development both in the affront to earlier federal promises and its almost complete disregard for the need to help Canada’s wine businesses escape from absurd post-Prohibition era regulation. It appears that the provinces view both Minister Anand and Prime Minister Carney as part-time comedians in respect of their promises of quick action. For the provinces … there is no rush, they are quite pleased to be involved in “glacial” reform efforts to address a problem, which they appear to have not thought about … even though it has existed for about a hundred years.

The remarks of Quebec Minister, Christopher Skeete, are telling (see Nine Provinces, Yukon Aim to Launch DTC Alcohol Sales by May 2026). He states that the provinces are “taking their time” to “ensure they get it right” regarding “something that’s never been done before in Canadian history”. For Pete’s sake … Canada is in serious trouble if we can’t solve an issue as simple as this one in a reasonable time frame. Minister Skeete (and the others) might wish to venture outside their walled alcohol fortresses and realize that this problem simply doesn’t exist in the rest of the world.

We simply need a national personal exemption for alcohol sales and shipment, just like most countries on Earth. Perhaps our new Prime Minister will eventually take offense and act at the federal level when he realizes that these provincial promises are not worth the memo (paper) that they are written on. Glacial provincial action on important issues is simply not acceptable in the current world. Is this comedy or tragedy? Perhaps both as far as the provinces are concerned.

We are now well past Canada Day, the date that the federal government had previously promised to remove our internal trade barriers regarding wine shipped and sold between provinces. We have no actual substantive progress to date – merely some vague announcements and promises to negotiate. It appears, unsurprisingly, that the government was too optimistic in thinking that the provinces would cooperate on this endeavour. This article explains the background to the relevant issues and why it will be hard to obtain meaningful provincial buy-in. As you will read below, the basis of the problem is the province’s reliance on liquor markup as a significant source of government revenue. In my view, this is one of the most significant long-term impediments to the health of Canada’s wine businesses.

1. What Are Liquor Markups?

In most jurisdictions, governments raise revenue from wine sales by imposing excise taxes at the wholesale level which are usually volume based. They may also include alcohol sales as part of their general sales tax systems which are usually percentage based. Many governments do both of these things, like Canada’s federal government which imposes a 5% GST on all wine sales as well as an excise tax which is currently set at $0.73 per litre. These taxes are relatively transparent because they are well publicized and need to be approved by Parliament.

However, the Canadian provinces take a somewhat different approach because each holds a statutory government monopoly over all liquor distribution within that province. As part of the ‘business operations’ of that monopoly, the province can impose ‘liquor markups’ on to all products sold within that province. These markups are not taxes so they do not need to be approved by each legislature. Often, they are not well publicized or transparent. Most commonly, the markups are calculated by adding a percentage based amount to the value of the product as a wholesale markup (e.g. in BC, the base markup is 89% of the supplier cost for wine). But sometimes, a volume based amount is added (e.g. in AB, the base markup on wine is $4.11 per litre). In some provinces like BC, there are both wholesale and retail markups, the latter of which are applied within government retail stores.

To a small extent, these liquor markups cover the costs of operating the liquor distribution system in each province. But mostly they are imposed simply to generate extra revenue for government. In other words, they are hidden taxes. What are the effects of and issues with this system?

2. Government Relies on the Hidden Tax Revenue

The first major effect is that each provincial government becomes dependent upon the liquor markup revenue that is collected by its liquor monopoly. For example in BC, the LDB sold $3.9 billion worth of liquor in its fiscal year ending in 2024. After deducting cost of goods sold, its gross profit margin was $1.7 billion. Operating expenses totaled $569 million for a net profit of just over $1.1 billion. In Ontario, the LCBO contributed $2.4 billion to provincial coffers for a similar time period. These amounts are a major contribution to provincial finances and make it difficult for government to objectively assess liquor policy reform.

3. The Markups Increase End Consumer Prices

The imposition of liquor markups increases costs throughout the supply chain. So if a monopoly imposes a high wholesale level markup (tax) on wine, the end consumer will end up paying a higher retail price for their bottle of wine. The extent of this effect varies considerably from province to province depending upon how they calculate and apply their markups. As a general rule though, because the liquor markups are designed to provide high amounts of ‘hidden tax’ revenue, the prices for wine in Canada are high compared to most of the western world and very high compared to other historic wine producing nations.

This poses a challenge for the development of wine and food culture both at retail and in hospitality (restaurants, bars, hotels). It also encourages black and grey market sales as consumers seek to buy at prices that are more competitive. Generally, the lowest markups on wine (particularly higher priced wine) have been applied in Alberta which uses a volume-based markup system described above. Provinces that use high percentage based markups (like BC) generally have the highest end-consumer prices.

The variability in markups is why wine prices differ so much from one province to another. In addition, most provinces except AB apply provincial sales taxes to wine, which generates additional revenue for government and further increases costs for consumers.

4. The Markups Discourage the Marketing and Promotion of Wine

The marketing and promotion of wine within the Canadian system is challenging because, generally, the provincial liquor monopolies apply their liquor markups to almost all wine products that move through their systems … even if those wines are being used for marketing and promotional purposes, rather than being sold to end consumers. This means that it is more expensive to promote and market wine in Canada than in other places in the world.

For example, even if a winery wishes to donate wine for marketing and promotion purposes (e.g. for a wine festival or trade fair), the importer will still have to pay the liquor markup. In most other places, any taxes/fees for such activity would be minimal but in Canada the liquor markups make it expensive to do such marketing. Historically, the only respite from this was to use ‘consular privilege’ (i.e. have the consulate from the wine producer’s country sponsor the marketing event and import the wine as consular wine) but this has become difficult if not impossible due to recent federal and provincial policy changes.

5. Creation of Exemptions from Markup for Local Producers

The existence of the markup system has proved to be detrimental to the development of Canada’s local wine industry. Canada’s domestic wine industry is young. Capital costs, land costs, and operating costs are high. This means that the base ‘supplier cost’ for wine produced in Canada is already high by global standards. If provincial liquor markups were added to that cost then, very frequently, the end consumer price for the wine would be too high and would be uncompetitive.

As a result, most provinces have felt compelled to provide local subsidies or preferences in order to encourage local industry. This has usually been done by reducing the effect of the markups on local wines either by exempting them from the markup entirely (BC) or by applying reduced rates of markup (ON).

While this has encouraged local industry, it has ancillary consequences: 1) In the local market, domestic wine is competing with imported products that are subject to higher mark-ups (and higher prices). While this benefits domestic wine, it makes it harder to export that same wine because as soon as the wine is outside the local market, it is competing with the same or similar wines that are priced much lower. 2) Most international trade agreements prohibit preferences which distort end consumer pricing. In contrast, direct subsidies aimed at agriculture or innovation are usually permissible. As a result, it is arguable that the approach of the provincial liquor monopolies is not trade compliant. Indeed, Canada has been found to violate some of our trade agreements for exactly this reason. These trade issues pose an ongoing threat to the system and to local producers. 3) Most provinces only provide their local preferences to their own provincial wine. Wine from other provinces is not provided with the same preferences. This is the main cause of our internal trade issues discussed further below.

Such issues become even more complex when unusual circumstances arise. For example, the recent climate related crop failure in BC has caused the BC Government to allow local wineries to obtain markup exemption even when they are using imported (mostly U.S.) grapes, which raises further trade compliance issues.

6. Problems with Inter-Provincial Trade

Each Canadian province has an alcohol regulation and distribution system that largely treats the other provinces (and their consumers) as if they were in foreign countries. As noted above, liquor markups are applied to wine from other provinces just as if that wine was imported from abroad. The regulatory structure is parochial in nature since there is virtually no recognition that other provinces’ Canadian wines should be recognized as ‘domestic’ product.

The heart of the problem is that each liquor monopoly maintains a ‘control’ mentality in order to ensure that it continues to collect the liquor markups that generate the large cash payments for its political overlords. Each monopoly is worried that its existence will be questioned if it is unable to maintain (and preferably increase) those payments. This is why most provinces still attempt to ban or restrict alcohol sales and shipment from other provinces … they are worried about losing their liquor markup revenue on those sales.

In this respect, markups have historically been worse than tariffs for the interprovincial trade in wine … because rather than creating a system that would permit the collection of the markup (and/or reducing the markups to more reasonable levels), the provinces instead made it illegal to make those interprovincial shipments … forcing wineries and consumers to break the law if they wanted to buy wine from another place within Canada.

A few provinces have changed their laws to some extent over the years. For example, Manitoba allows all such interprovincial shipments and has done so since 2012 when the federal law changed. BC and Nova Scotia allow such shipments if they consist of 100% Canadian wine and are shipped from the producing winery. Saskatchewan and Alberta allow the shipments if the markup is collected using complex permitting systems. But in the latter case, and as of April 1st, the Alberta government has moved from a relatively simple flat rate system to a more complicated one with higher markups that is going to be challenging for both wineries and consumers to accept. The other provinces and territories still maintain blanket bans.

This is a ludicrous situation which completely holds back the development and expansion of Canadian wine businesses by preventing consumers from patronizing any such business that is not located in their home province. Imagine if it was illegal for someone in Paris to purchase wine from a winery in Bordeaux? Or against the law for a consumer in Rome to buy wine from Tuscany?

In this respect, it is important to note that Manitoba (the only fully open province in Canada right now) has reported no problems with their open borders policy and has seen no appreciable drop in liquor markup revenue as compared to other provinces.

7. Reform of Liquor Markup System

The above discussion highlights the issues with the implementation of and the reliance upon liquor markups by the various provincial governments. In an ideal world, it would be beneficial to re-think this system and come up with something better. However, this will be challenging. Here are some ideas and reasons why it will be tough.

A. Switch from percentage based markups to volume based markups.

Most wine producing jurisdictions use volume-based excise taxes to raise money from alcohol sales. Alberta’s volume-based markup system was the envy of the Canadian wine business until recently. For about 3 decades, Alberta’s approach created a vibrant retail and hospitality market for wine with reasonable prices, great consumer selection and consistent government revenue. About a year ago, the system was also extended to allow DTC sales for BC wineries (upon payment of the markup – about $3 per bottle). This would have created a smart national precedent for a workable and relatively open system. Unfortunately, Alberta has recently backtracked (in the hope of raising more money) and introduced an additional percentage based liquor markup on “high value” wine which will raise consumer prices and which makes the DTC system so complex that it is unworkable.

In my view, it would make more economic sense (and create a healthier wine marketplace across the country) if the provinces all switched to volume based markups (and for AB to switch back). However, this is a fundamental change which would require considerable work within the liquor monopolies.

B. Realistic levels for the markups

Liquor monopoly sales are falling due to reduced consumption. It’s unlikely that the monopolies can meaningfully reduce their operating expenses. This means declining revenue for government unless the system is restructured. At the present time, the percentage based markups are simply too high and it’s hard to increase them. They create consumer resistance, stifle the growth of food/wine culture, hurt hospitality/retail businesses, and encourage grey or black market sales. The imposition of volume-based markups at a reasonable level would restore overall health to the system … and enable government to maintain revenue without adversely affecting end consumer prices.

In addition, the use of percentage based liquor markups on trade samples and wine imported for marketing purposes actively discourages the promotion of the wine business and the development of wine culture. A volume-based system would make such costs more reasonable.

C. Some Commonality of Markup Levels Would Solve the Internal Trade Issues

If the provinces switched to volume-based markups en masse and at a relatively consistent tax level, there would be little incentive, between provincial marketplaces, for consumers to buy in a different province. This would enable the provinces to accept a personal use exemption for all interprovincial wine sales, either free of markup for all such transactions or at a commonly agreed upon reasonable level.

****

However, government’s quest for more money and continued control will probably over-ride all these concerns as we have recently seen in Alberta. In addition, how likely is it that the provinces can be persuaded to adopt blanket and more consistent pricing reforms … and mostly at the same time? The unfortunate reality is that bureaucratic opposition and political inertia will likely doom any significant reform efforts … and that the best we will see is a half-baked DTC system in a few provinces that is too expensive and complicated to work.

It remains my view that the only real likelihood of change is for the federal government to legislate a solution as I previously explained in an earlier post (last two paragraphs of DTC Canada vs USA – a Tale of Unfortunate Contrast): the federal government should exercise its exclusive jurisdiction over interprovincial trade and legislate a national personal exemption amount for interprovincial wine sales. Yes, the provinces would probably object (and might go to court) … but as we have seen from Manitoba, there would be little significant effect in the long term … and once the gates are open, they will likely stay open.

Canadians deserve much better than the absurd status quo on this issue … and it is long past time for Canada to “free its wine”.